When you try to turn your Bitcoin or Ethereum into cash in Russia, your bank doesn’t just process the request - it flags it. Since September 2025, Russian banks have been under strict orders from the Central Bank of Russia (CBR) to treat any crypto-to-fiat withdrawal as a potential threat. It’s not about suspicion of crime - it’s about control. The system is built to slow you down, question you, and sometimes freeze your cash for two full days - no warning, no explanation, just a message on your phone saying your withdrawal limit dropped to 50,000 rubles (about $600).

Why This Rule Exists

Russia isn’t banning crypto. It’s trying to contain it. The government admits that over a third of all cross-border money leaving the country now flows through cryptocurrency. That’s a problem for a nation under international sanctions, where controlling capital flight is a top priority. The CBR’s own data shows that 273,100 scams in just the second quarter of 2025 were tied to crypto withdrawals - totaling over 6 billion rubles. That’s the official reason. The real one? They want crypto transactions to go through their channels, not around them.

So they didn’t just make a rule. They built a surveillance system. Banks now monitor 12 specific patterns that trigger automatic restrictions. If you withdraw cash at 2 a.m., use a QR code instead of a card, or get a large transfer and withdraw it within 24 hours - your account gets flagged. Even small things matter: if your phone suddenly starts receiving 3+ messages from unknown numbers before you withdraw, that’s enough to lock your cash.

What Happens When You Withdraw

Imagine you sold 200,000 rubles worth of crypto on a peer-to-peer platform and tried to pull the cash out of an ATM. Within 15 minutes, you get an SMS: "Your daily withdrawal limit is now 50,000 rubles for the next 48 hours." You can’t touch the rest. Not even 10,000 more. You’re stuck.

This isn’t rare. Users on Russian forums like BitBoom and Reddit’s r/RussianCrypto report this happening constantly. One user, "CryptoTrader89," had his Sberbank account frozen for 72 hours after withdrawing 65,000 rubles from a Paxful trade. He had to show up in person with screenshots of his wallet, transaction IDs, and even proof that the buyer was a real person. No one asked him if he was laundering money. They just asked: "Where did this money come from?"

And the banks aren’t just being cautious - they’re overloaded. Sberbank alone hired over 200 new analysts just to monitor crypto-related transactions. Processing a flagged withdrawal now takes nearly 19 hours on average - up from under 3 hours before September 2025. If you’re not in a rush, you might wait. If you need cash for rent, medical bills, or groceries - you’re out of luck.

The Hidden Cost: How Traders Adapt

People aren’t giving up. They’re adapting. The most common workaround? Using multiple bank accounts. Active crypto traders in Russia now hold an average of 3.7 different accounts. They stagger withdrawals - one bank on Monday, another on Wednesday - hoping to avoid triggering cross-institutional monitoring. It’s risky. If the system notices you’re moving money between accounts to bypass limits, it can trigger even stricter reviews.

Another tactic? Building "natural" transaction histories. Experts recommend having at least three months of regular spending - grocery runs, utility payments, Netflix subscriptions - before even attempting a crypto withdrawal. Banks are trained to spot sudden, unnatural patterns. If your account sat empty for months, then suddenly received 500,000 rubles from a crypto exchange, that’s an instant red flag. But if you’ve been paying your phone bill for 90 days and then withdrew 40,000 rubles? Less likely to get blocked.

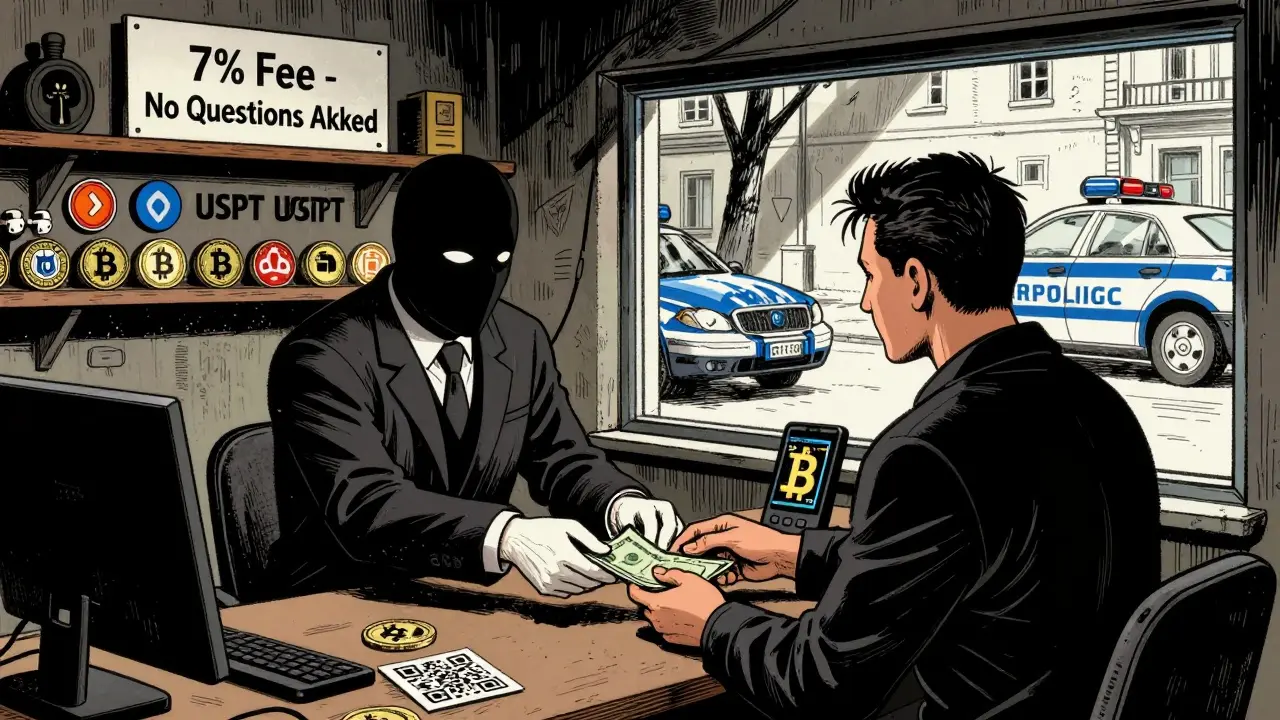

And then there’s the underground economy. With official channels slowing down, unregulated exchange offices have popped up in Moscow, St. Petersburg, and Kazan. These places take crypto - Bitcoin, USDT, even Monero - and hand over cash. But they charge 7% to 12% in fees. That’s not profit. That’s a tax on freedom. And it’s growing. Rosfinmonitoring, Russia’s financial monitoring service, reported a 22% spike in unregulated crypto activity in the first three weeks after the new rules went live.

The Double Standard: Crypto for Trade, Not for You

Here’s the twist: Russia doesn’t hate crypto. It just hates you using it. The government has quietly approved a path for banks to handle cryptocurrency - but only for big business. In October 2025, the CBR announced that domestic banks could hold up to 1% of their regulatory capital in digital assets - as long as they keep 150% reserves. That’s not a loophole. It’s a controlled pipeline.

And it’s not for personal use. This is for international trade. Russia wants to pay for oil, grain, and metals with crypto - but only through state-approved channels. The digital ruble, launching in phases starting September 2026, will be the official tool. Private crypto? Not so much. The central bank is testing blockchain systems for commodity exports with five major banks. Meanwhile, if you try to cash out your Dogecoin to buy a new phone? You’ll get locked out.

What’s Next? The Road to Total Control

The restrictions aren’t done. By December 1, 2025, banks will be required to verify the source of any crypto withdrawal over 100,000 rubles. That means not just screenshots - you’ll need notarized records from exchanges. Good luck if you traded on a decentralized platform like Uniswap or LocalBitcoins. They don’t issue receipts. They don’t keep logs. And now, the bank won’t accept your word.

Worse, legislation is moving through the Russian Duma that could make repeated violations a criminal offense. First offense? Fine. Second? Jail. Up to 5 years. If you’re part of a "organized scheme" - whatever that means - you could face 10 years. No one knows exactly how they’ll define "organized." But they’re building the system to catch you anyway.

Final Reality: You’re Not a Customer. You’re a Risk.

Russian banks don’t see you as a client. They see you as a potential violation. Your wallet address, your transaction history, your ATM location - all of it feeds into a machine that’s designed to say no. The goal isn’t to stop crime. It’s to stop autonomy. To force every crypto transaction into a box the state can watch, track, and control.

If you’re living in Russia and using crypto, your options are clear: accept the limits, pay the underground premium, or stop using cash altogether. There’s no middle ground. And as the digital ruble rolls out in 2026, that gap will only widen.

Can I still withdraw crypto to fiat in Russia without getting blocked?

Yes - but only if you avoid triggering the 12 flagged behaviors. Stick to small, regular withdrawals under 50,000 rubles. Use the same bank account for consistent, non-crypto spending for at least 90 days. Avoid withdrawing after midnight, using QR codes, or receiving large transfers right before cashing out. Even then, there’s no guarantee. The system is designed to catch you.

Why does the bank care where I got my crypto from?

Because Russia doesn’t want crypto circulating freely. The government sees unregulated crypto as a threat to its control over money. By forcing you to prove your source, they’re creating a paper trail that ties every transaction back to an approved channel. If you can’t prove it, they assume it’s illegal - even if it isn’t.

Is it safer to use a different bank for crypto withdrawals?

Not really. All 347 licensed banks in Russia are required to follow the same CBR rules. Sberbank, Tinkoff, VTB - they all use the same monitoring software. Switching banks might delay the block, but it won’t prevent it. In fact, using multiple banks can make things worse - the system looks for patterns across institutions, and that’s an instant red flag.

What happens if I ignore the 50,000 ruble limit and keep trying?

You’ll get locked out longer. After the first 48-hour block, if you keep trying, the bank will escalate. You may be asked to visit a branch for identity verification, provide notarized documents, or even be flagged for anti-money laundering review. Repeated attempts can lead to account suspension or mandatory reporting to Rosfinmonitoring. Don’t test the system - it’s designed to win.

Can I use a crypto debit card to avoid these restrictions?

No. Cards linked to crypto wallets - even those issued by Russian banks - are treated the same as direct withdrawals. The CBR’s directive includes QR code usage and virtual card spending as high-risk behaviors. If you use a crypto card to pay for groceries or gas, that transaction can still trigger the 50,000 ruble limit if it’s flagged as unusual. There’s no work-around.

Are there any legal ways to convert crypto to cash in Russia right now?

The only legal path is through state-approved channels: selling crypto on licensed exchanges that report to the CBR, then withdrawing the fiat through your bank account. But even that’s risky. The exchange must have a license, and your bank must not flag the transfer. Most P2P trades, even with verified users, are still considered high-risk. There is no truly safe way - only less risky ones.

Final Thoughts

Russia’s approach isn’t about security. It’s about power. The banks aren’t protecting you - they’re protecting the state’s control over money. If you’re trying to move crypto into cash, you’re playing a game with rules that change daily, written by people who don’t trust you. And the longer you play, the harder it gets.

Sarah Hammon

March 19, 2026 AT 14:10iam jacob

March 19, 2026 AT 21:55Diane Overwise

March 20, 2026 AT 12:15Ann Liu

March 21, 2026 AT 06:14Dionne van Diepenbeek

March 22, 2026 AT 07:10